Exponentially growing screen time coupled with increased privacy restrictions and economic pressures of the softening economy pulls many media businesses toward the ad-supported model.

This year we witnessed the onset of new ad networks, Marriott, Netflix, and Xbox, any company with sufficient size and scale of data wants to build an ad network. Programmatic is a preferred method for entering the ad trade for newcomers. Standardized, interoperable marketplaces allow new ad networks to quickly scale and access the global demand.

A brief AdTech industry overview suggests that programmatic is consolidating its positions in maturing media formats, like CTV, DOOH, in-game, and digital audio. At the same time, despite the uncertainty caused by the approaching ad ID deprecation, programmatic is standing its ground with emerging semantic solutions, first-party data infrastructure, and ID tech. The mounting challenges in the in-app and web environments compel ad companies to consolidate and increase their technological footprint, causing the DSP/SSP disintermediation and rise of the in-app and in-game ad titans.

Let’s review which AdTech trends will extend into the next year and will be relevant for AdTech companies, media, publishers, and agencies looking to build new technology in 2023.

Onset of first-party data infrastructure

Google has delayed the end of third-party cookies again. What was originally planned for Q2 2022 was deferred to 2023 and is now shelved till 2024. Cookie deprecation delay or not, the industry is entering the first-party data era.

The Privacy Sandbox will need a lot of tweaks to be an effective ad identifier and achieve regulatory blessing. Google will likely be strongarmed into offering fewer comprehensive cohorts for targeting — which won’t compensate for third-party cookie deprecation. AdTech needs to agree on and implement a high-level solution based on a sustainable universal ID, first-party infrastructure, and transparent consent mechanisms for sharing data.

As browser- and device-supplied knowledge is fading out, first-party data and user intelligence are becoming the new lifeblood of AdTech. SSPs and DSPs, capable of securely processing bid requests with first-party data, will command a bigger share of the advertising market. SSP/DSP-owned data clean rooms and deep integrations with major cookieless solutions can be a solid offering for prominent brands. At the same time, integrating with existing players can make your ad business more attractive to customers.

Convergence of SSP and DSP

In this landscape of data scarcity, mobile DSPs and SSPs are forced to adjust to new technologies, integrations, and perhaps even expansion to previously untapped business models. The lines between buy- and sell-side AdTech companies have become increasingly blurred. Earlier this year, The Trade Desk, the industry’s largest independent DSP, proposed direct integration with premium publishers via its OpenPath initiative, a move many interpreted as an immediate threat to the traditional role of SSPs.

On the other hand, SSPs are increasingly forming partnerships with media agencies— relationships that DSPs traditionally facilitated. For instance, PubMatic, a formerly old-school SSP, reported that it made more than a quarter (27%) of its Q4 2021 revenue from helping advertisers buy better impressions. Another well-known example is Integral Ad Science, an ad verification firm at the core, but its latest move has it operating more like a large SSP.

In 2023, programmatic platforms would have to diversify their business model and create a holistic ecosystem that connects buyers, sellers, publishers, data platforms, and everything else in between in a way that’s efficient, transparent, data-rich, and equipped with ad fraud detection. SSPs must consider rolling out capabilities for the buy-side with custom DSP development. At the same time, the ad platforms with access to premium inventory would benefit immensely from the development of their own SSP.

Top AdTech companies invest in contextual advertising

With behavioral targeting leaving the center stage, contextual targeting is back in fashion. However, advertisers are not ready for a broad categorization of CPM networks. They need the new context quality — comprehensive reporting, predictive analytics, and ultra-narrow targeting.

As a result, the market is desperately looking to develop new programmatic tools, from AI-based predictive marketing platforms to various contextual solutions. Many players that were originally in the behavioral targeting business, like Captify, Criteo, and Silverbullet, switched gears and are now heavily invested in contextual alternatives. Get ready to see a raft of newcomers as well as headline-worthy funding rounds in this space this year.

For big-name publishers with diverse content verticals, contextual advertising is a proven way of generating revenues without the bother of extra tech. The Washington Post and The New York Times have used this technology for ages. It’s a huge industry, worth $157.4 billion in 2020 and projected to hit $335 billion by 2026.

The modern ML-based contextual solutions for CTV also allow advertisers to run data-driven contextual campaigns on Smart TVs based on the behavior of the existing audience, scale it, and create look-alike segments.

The major AdTech trend in 2023 is contextual advertising platforms that can identify context through different lenses — semantics, video, and user behavior metrics — then provide advertisers with rich metrics for cookieless targeting, audience activation, and engagement.

Rise of CTV measurement

CTV ad spending is set to increase from $14.11 billion in 2022 to $18.29 billion in 2024. As Netflix and Disney+ (among many others) launch ad-supported tiers, ad inventory will also grow in volume.

However, media buyers have mixed feelings about CTV advertising. Over $1 billion in ad budgets is wasted on running ads when the CTV sets are off.

Generally, CTV (connected TV) advertising is perceived as difficult to measure. However, with the right tech stack and integrations, connected TV ads can be tracked with precision almost equal to other digital channels. The IP addresses and device graphs can be coupled with the advertiser’s first-party data, syndicated research, and segmentation to reinforce the targeting.

ML-based creative optimization can give a huge boost to CTV advertising: contextual engines that monitor the metadata sources and can recommend the best music, visual material, and messaging tactics to approach a viewer. These technologies can revolutionize CTV (connected TV), extending the shelf life of the video ads and allowing to them to be customized on the fly for specific audiences automatically.

Brands are eager to test the multiple CTV attribution options on the table. The Trade Desk, Verizon Media, and Viant Technology already went with iSpot. Xandr, ABEMA, and Smadex, tvScientific have selected Adjust.

To boost interoperability in this environment, IAB Tech Lab recently expanded measurement with OM SDK to CTV. It is a major step forward in simplifying the verification across screens and bringing consistency and transparency to the CTV industry. In 2023, we will see a swift adoption of the OM SDK standards among publishers and an onset of attribution platforms that account for CTV audiences.

Supply chain transparency

IAB Tech Lab announced the finalization of the OpenRTB 2.6 draft and reported that the new standard is ready for implementation. With the new version, both supply and demand sides get more flexibility, especially in the CTV and context. The new protocol accounts for the lags of the old version that prevented effective media trading of the swiftly maturing streaming inventory.

The IAB Tech Lab has also released Ads.txt 1.1. In the new spec, IAB adds values to help buyers determine the owner and manager of inventory. The update includes two new values for publishers to declare within their ads.txt files, “owner domain” and “manager domain,” to help reduce fraud. Ads.txt is regularly abused by publishers, mismarking their relationships with exchanges and resellers. These two ads.txt variables are tailored to ensure that all three field values can be validated.

In addition to updating the industry standards, IAB Tech Lab announced the launch of the Transparency Center — a public database for companies within the digital advertising supply chain to share information about their audience segments. The repository contains structured metadata about publishers, ad tech intermediaries, and buyers in explorable and downloadable format.

Transparency Center crawler performs full-scale crawls of ads.txt, apps-ads.txt, and seller.json. A self-attestation program allows companies to publicly declare which IAB Tech lab specification and version they use in the production environment. AdTech trends 2023: the full-scale implementation of the Transparency Center can potentially once and for all put an end to supply-chain fraud and misrepresented inventory, a giant leap for accountable programmatic trading.

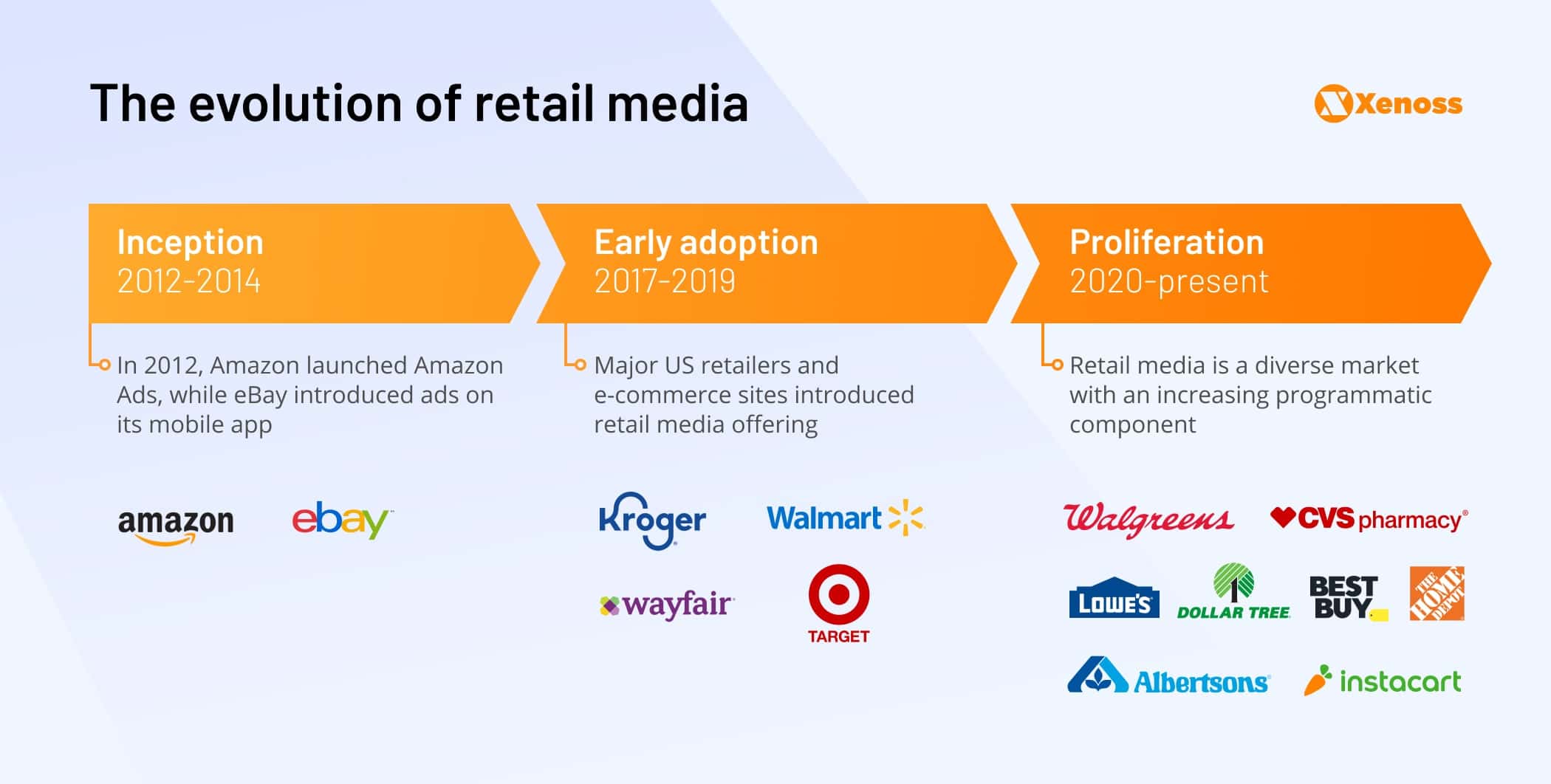

Programmatic retail media networks

Many retail media networks work as closed-loop ecosystems; e-commerce sites provide their advertising partners or agencies they contracted with a self-serve interface to place ads only on their inventory.

However, retail media networks increasingly employ a programmatic approach, where retail media inventory is connected to off-site properties and third-party media for omnichannel reach in retail campaigns.

For instance, Walmart recently partnered with the Trade Desk to launch its own DSP, allowing its advertisers to serve ads on the programmatic inventory and its retail media placements Despite the partnership with The Trade Desk, Walmart is using the WL-cloned version of TTD without access to its wider infrastructure. With its own supply-side tech, it is basically a walled garden.

Target has an exclusive SSP partner and is open to outside DSPs, with recently connected CitrusAd, Criteo, Skai, and Pacvue. Kroger has an open PMP program with access to third-party DSPs. Pacvue, Skai, and Flywheel Digital were the first to connect. Instead of creating a proprietary network, other retailers partner with existing retail media solutions, such Criteo and CitrusAd, that group the inventory of different retailers to provide an extensive reach for brands and advertisers.

DOOH coming of age

Globally, 76% of marketers plan to increase DOOH (digital out-of-home) advertising budgets in 2023. In the US, DOOH ad spending is projected to reach $367 million by the end of the year, up by 15% compared to 2021.

Much of the industry growth will come from rapid programmatic DOOH expansion, with RTB opportunities now becoming available via mainstream DSPs. Google has made digital out-of-home (DOOH) ads available to all users of its advertising marketplace Display & Video 360 (DV360). Google’s DV360 already currently partners with various DOOH SSPs and ad exchanges such as Hivestack, Magnite, PlaceExchange, Ströer SSP, VIOOH, and Vistar Media, which give access to major out-of-home media owners’ inventory, including ClearChannel, JCDecaux, Intersection, Lamar, and Ströer.

Programmatic DOOH is only at the beginning of digitalizing OOH, an uncharted new territory to conquer. It comes with a host of obstacles, mainly around data processing, ad viewability measurement, and low-latency ad creative processing. But those that resolve these issues will be well-positioned for upcoming growth.

In 2023, advertisers will look to scale beyond private marketplace deals and programmatic guaranteed ad placements. Many also want to run dynamic, data-rich campaigns in locations frequented by their ideal targets. But few players deliver that type of end-to-end buying experience. Maybe, the DOOH (digital out-of-home) newcomers will be able to fill in this gap.

Overall, the DOOH market is merely entering the growth stage. Over the next two years, 95% of advertising executives expect the DOOH (digital out-of-home) market to grow significantly and surpass $50-$55 billion by 2026.

Ready to add programmatic DOOH capabilities to your platform?

In-game advertising boom

In-game advertising is a promising new pocket of growth for programmatic, specifically the rise of native in-game advertising. For the first time since 2009, the Interactive Advertising Bureau (IAB) has released updated guidelines for intrinsic in-game advertising, also known as in-gameplay or native in-game advertising. This year, a lot of potential entries announced their interest in this ad environment.

For once, Microsoft is building a platform to let brands advertise in Xbox F2P games. The company intends to create a “private marketplace” where only select brands can insert ads into games in a way that doesn’t disrupt the gameplay experience. Xbox currently allows limited forms of advertising. Right now, advertisers can buy in-game ads on certain games from the top in-game advertising companies.

All major gaming companies will eventually create their own ad networks; Sony’s PlayStation and Amazon’s Twitch have already voiced their plans in this regard.

At the same time, media agencies are growing increasingly fond of this type of advertising and hastily brokering necessary integrations. Recently, WPP partnered with Epic Games to provide brands with an interactive advertising experience in Metaverse. It is an important milestone for AdTech and the broader adoption of in-game advertising in AAA games, which brings to light the immense opportunities of this medium for brands.

Innovative games like Fortnite are creating an entire cottage industry of creative agencies developing new advertising formats in the metaverse that blend with other game monetization formats, as demonstrated by in-game events, exclusive appearances, and even fashion brand collaborations for game-themed virtual reality merchandise.

In-app consolidation

In-app advertising is on everyone’s radar, especially now when Unity rejected AppLovin’s historic $18 billion takeover bid to go ahead with its ironSource buyout and develop its own ecosystem.

With the broken CPI measurement on Facebook, it is critical for app publishers to consolidate or in-house their AdTech stack, as most market players use various solutions for analytics and attribution, which don’t exchange data. Publishers should prioritize their own ad demand as ad networks take a significant cut in the game monetization supply chain.

Major players like AppLovin, Liftoff+Vungle, and Unity+ironSource have already created their ad networks or launched DSPs, mounting their walled gardens.

Also, Apple is building its own DSP. It seems that Apple’s recent push for privacy was just aimed at eliminating the AdTech competition and building the walls of its own walled garden.

In a short while, we will get a DSP for the Apple ecosystem. This is easily going to reach $10s of billions in a short period of time.

Google’s upcoming restrictions around ad placements in Android apps can also spur consolidation in several app categories, such as hypercasual games. In a nutshell, the recent Android updates are phasing-out interstitial ads — the main instrument of ad-supported monetization in this environment.

Going forward, app developers will be forced to reassess their ad placement choices and prioritize ad formats that don’t disrupt the user experience and interfere with normal app use or gameplay. In 2023, rewarded ads and native banners will dominate this environment, and some innovative AdTech companies like YOC, ensuring engaging and non-disruptive advertising experiences, will immensely benefit from this trend. Also, new innovative ad formats can take hold in the market, such as audio ads.

Podcast ads

Podcast CPMs rose to $26 in the third quarter of 2022, up from $22 for the same period in 2021, rising above streaming TV ad costs.

The rise in CPMs is propelled by the privacy changes in the AdTech space, which impact mobile device ID and third-party cookies and don’t directly impact podcasting.

Over the past two years, the industry’s major players have acquired companies like Megaphone, which focused on one feature: inserting ads into podcasts. With the recent wave of acquisitions, you can now reach 50% of weekly listeners in the US by advertising on just four podcast networks: Sirius XM Media, Spotify, iHeartRadio, and NPR.

The unique data landscape in podcast ads makes vital partnerships with the right third-party attribution vendors. In 2023, we will likely see a wave of partnerships between digital audio companies and programmatic media platforms that can match the listener to their unique data set and find data on that user that also includes the IP address to link that ad exposure to conversion.

Sustainability

Media buyers and publishers are seeking ways to reduce their carbon footprint. Reducing emissions requires changes to parts of the business, including the supply chain, product production, and capital investments. For marketers, most of these emissions can be improved by improving energy efficiency – reducing the energy required to run a platform through more efficient technology.

The AdTech industry is particularly important in reducing Scope 3 emissions. Brands and publishers need to work with sustainable companies to meet their goals. Brands work with a variety of technology companies, data providers, and agencies, all leaving their carbon footprint. The entire industry is being tested to become more sustainable.

AdTech trends going strong on the eve of 2023

In 2023, programmatic advertising is going through a transformative period with the shift to privacy-first advertising and the deprecation of ad IDs at the forefront. Adopting industry standards, factoring in contextual signals, and developing transparent data exchange mechanisms will be critical for the industry to adapt and thrive.

First-party data infrastructure will be crucial for effective brand advertising. And tapping into growing segments such as CTV, DOOH, digital audio, and gaming could be the key to programmatic marketing moving into 2023. Being agile and constantly updating your data and attribution capabilities, together with proactive integrations, will be essential.