- Solutions

- Capabilities

- Industries

- Resources

- About

-

-

- Enterprise AI agents

- Enterprise multi-agent systems (MAS)

- AI chatbots and co-pilots

- Enterprise knowledge management

- Recommendation engines

- AI image and video generators

- AI sound generators

- Fraud detection systems

- Intelligent Process Automation (IPA) systems

- Enterprise business intelligence platforms

- Root cause analysis (RCA) tools

-

-

-

- Data pipeline engineering

- Data stack integration

- Enterprise application modernization services

- Data migration

- Data observability & quality platforms

- Data fabric

- Data infrastructure

- Data mining and preparation

- Infrastructure cost optimization

- Real-time data solutions

- Data analytics solutions

- Data visualization & reporting solutions

- Data strategy

- Data engineering consulting

- Data labeling

- Business intelligence

-

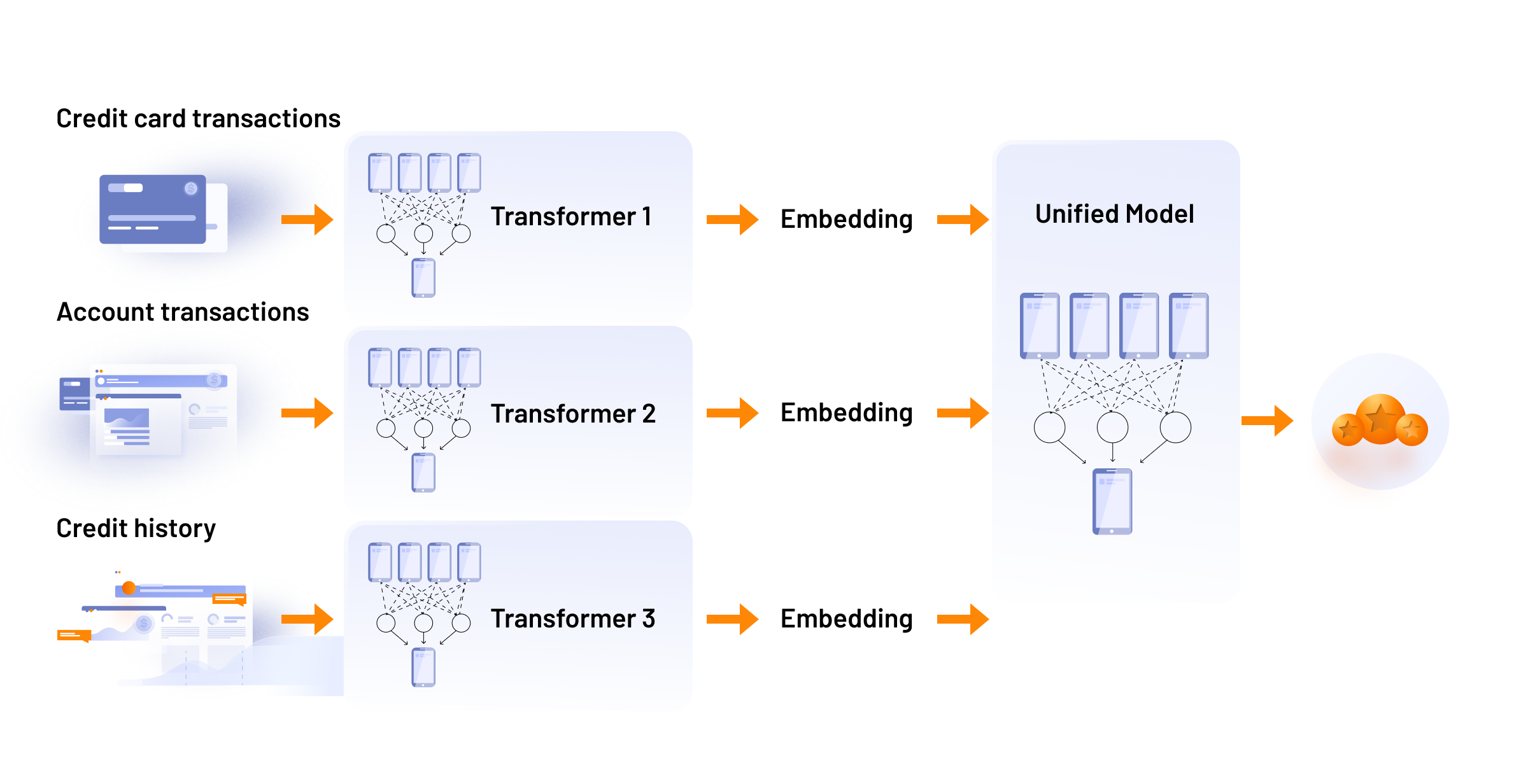

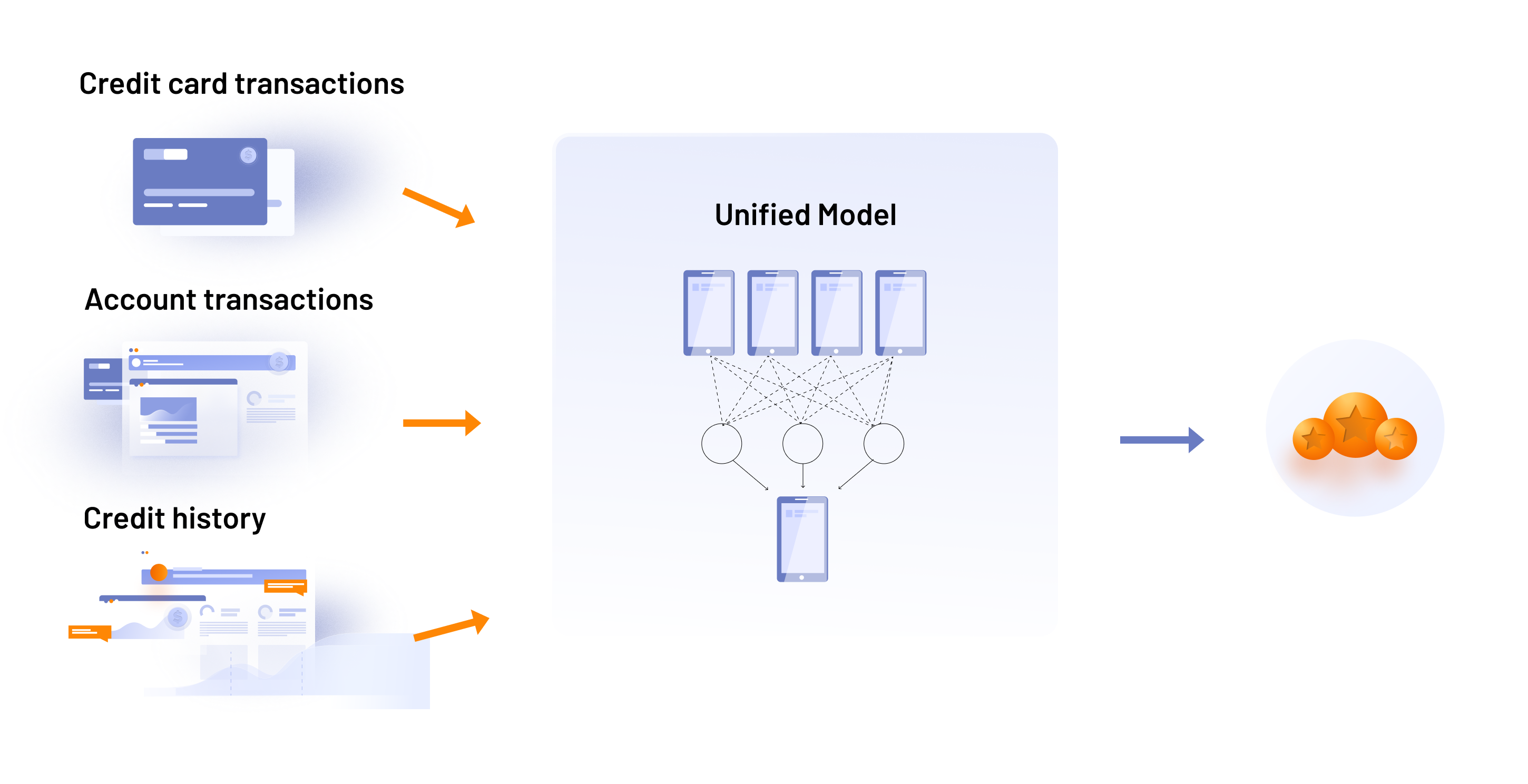

- Fraud detection & risk scoring

- Time series forecasting development

- Predictive maintenance systems

- Churn prediction development

- Demand forecasting systems

- Customer segmentation engineering

- Dynamic pricing systems

- Recommendation engine development

- User conversion prediction

- CTR prediction pipelines

- RTB auction win price prediction

-

- Data labeling for computer vision

- Robotic automation

- Image labeling, analysis and segmentation

- Object detection and tracking

- Face and person recognition

- Intelligent video and character recognition

- Audience measurement for DOOH and Connected TV

- Contextual ad placement in in-game and video advertising

- Brand visibility and exposure analysis

- Sentiment analysis in UGC ads

- Influencer brand fit evaluation

-

-

-

- AI for advertising

- SSP and Ad Network development

- DSP development

- Connected TV (CTV) and OTT advertising platforms

- Programmatic DOOH advertising platform development

- Ad fraud detection and prevention software development

- Custom advertising solutions for publishers

- Retail marketing technology

- Custom in-game advertising solutions

- Customer data platform development

- Autonomous AI agents

-

-

-