This article is the first in a three-part series on how insurers can use AI to transform claims operations. Here, we’ll start by unpacking where and why claims break down today.

- In Part 2, we’ll spotlight specific, high-impact AI use cases across the contact, investigation, and settlement phases.

- In Part 3, we’ll offer a playbook for senior leaders to futureproof claims organizations and steer transformation with confidence.

The insurance industry is staring down a talent crisis. In Q1 2025, 55% of carriers reported plans to increase headcount over the next 12 months. The area with the highest demand? Claims. It’s not hard to see why: the process is slow, manual, fragmented, and increasingly out of step with policyholder expectations.

Claims are the beating heart of customer experience in insurance. It’s where trust is earned—or lost. And right now, that heart is under serious stress.

Why insurance claims processes are failing

Let’s cut through the noise. Most insurers know their claims processes are inefficient. But what’s actually driving the friction?

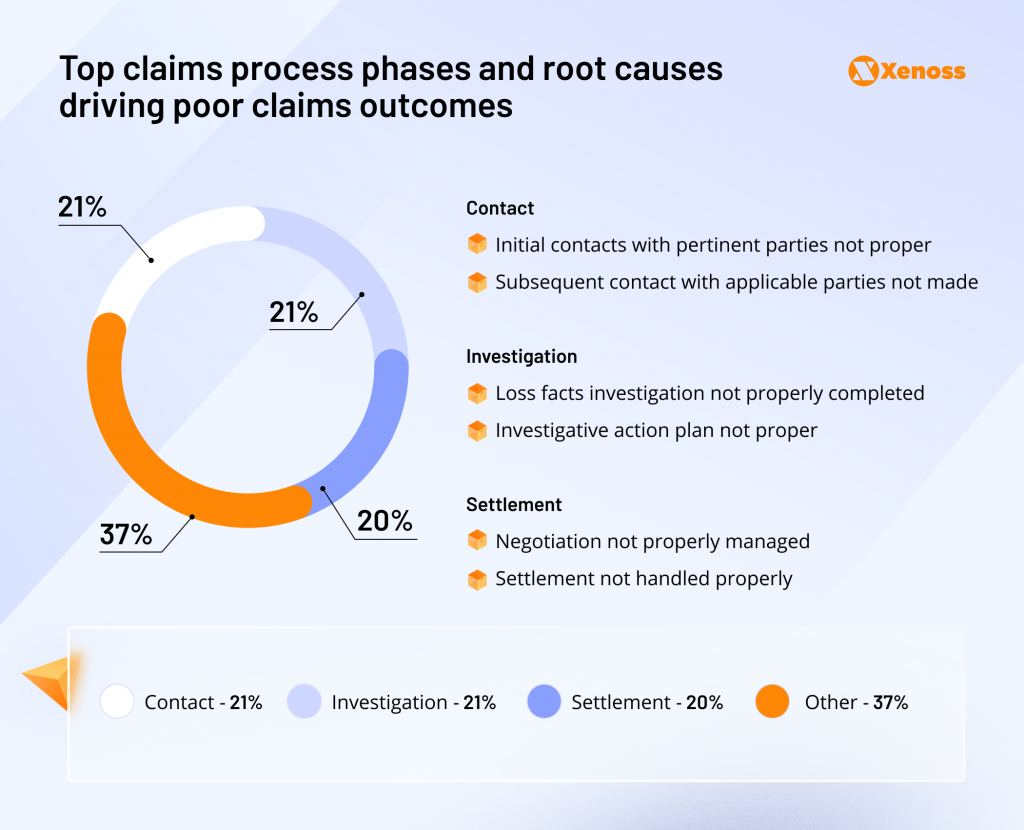

To find out, Aon’s Strategy and Technology Group (STG) benchmarked over 100 claims operations. The analysis revealed that most quality breakdowns occur in three core phases: contact, investigation, and settlement.

These aren’t obscure edge cases—they’re structural flaws rooted in communication, workflow, and execution. Let’s break each one down.

1. Manual and disjointed claims workflows

From first contact to final settlement, claims departments still lean heavily on paper, siloed systems, and labor-intensive tasks. The result? Delays, errors, and inconsistent experiences.

As highlighted in Riskonnect’s analysis, overburdened adjusters are juggling high caseloads without the tech support they need. Meanwhile, N2uitive flags workflow fragmentation and lack of centralization as root causes of leakage.

Manual process = brittle process. Every handoff becomes a potential break point.

2. Poor claims communication

Digitizing intake is a step forward, but policyholders may feel overlooked or left in the dark without timely follow-ups. According to the J.D. Power 2024 U.S. Auto Claims Satisfaction Study, the #1 driver of satisfaction isn’t app design or payout size—it’s how easy it is to communicate with reps.

That insight is echoed in a customer behavior report by EasySend. Clear, proactive communication is one of the top three things customers want improved. And yet, it’s one of the most common gaps in execution.

3. Insurance fraud is alive and well

Let’s talk about the elephant in the room: fraud.

According to Insuresoft, up to 20% of all claims could be fraudulent. That’s not just an operational issue—it’s a bottom-line threat. Ineffective fraud detection means higher loss ratios and unnecessary payouts. It also slows down legitimate claims, turning your best customers into frustrated ones.

Modern fraud requires modern defenses—data modeling, behavioral analytics, and real-time validation. Unfortunately, many carriers are still stuck with outdated checks or rely too heavily on human intuition.

4. Claims cycle time to settle is still too long

Cycle time is one of those metrics that’s deceptively simple. Everyone wants to reduce it, but few understand where the delays actually come from.

The 2024 J.D. Power study notes that while some progress has been made in auto repair timelines, the total time to resolution remains a key pain point. For many claimants, that means waiting weeks—sometimes months—for reimbursement or closure.

That delay erodes satisfaction, increases inbound call volume, and triggers unnecessary escalations. It’s a vicious loop—and it’s not sustainable.

The insurance talent crisis: Why claims teams are struggling

Even the most advanced system needs qualified humans to run it. And right now, those humans are in short supply.

According to Idex Consulting’s 2025 Salary Guide and Sentiment Report, 52% of insurance employers admit they don’t currently have the talent needed to meet business goals. Even worse, 76% are planning to hire in the coming year—but many won’t find the people they need.

Why?

- 72% of insurers report challenges finding staff with the right data and tech skills.

- The workforce is aging fast—Dominion Risk and Accenture both note a growing exodus of experienced employees.

- Turnover has jumped from historical norms of 8–9% to 12–15%, according to Deloitte.

You’re seeing more work, fewer people, and steeper learning curves. That’s a recipe for burnout—and it’s already playing out in claims centers nationwide.

Automation isn’t optional anymore

The old model—hire more adjusters, add more paperwork, and hope for the best—doesn’t scale. If insurers want to stay competitive, they need to think like tech companies.

That means:

- Workflow automation to handle repetitive tasks and triage low-severity claims.

- Integrated communication systems that centralize messages across email, text, apps, and phone.

- Fraud analytics tools to flag risky claims in real time, not after the fact.

- Digital-first reporting that makes the customer feel informed and in control.

Automation doesn’t replace people—it frees them to work smarter. Think less keyboard-pounding, more strategic problem-solving.

Rebuilding trust, one claim at a time

Here’s the brutal truth: policyholders don’t care about your org chart or your legacy systems. They care about one thing—whether you show up when it matters.

Claims are where that promise gets tested. And today, the test is getting harder.

To win in 2025, carriers need to:

- Modernize fast, without compromising compliance.

- Hire for data fluency, not just domain experience.

- Invest in communication—because silence feels like abandonment.

- Treat claims as a customer retention engine, not just a cost center.

Coming next in the series:

In our next article, we’ll break down where AI can realistically improve each of the three core claims phases: contact, investigation, and settlement. Expect real-world use cases, implementation tips, and a framework for evaluating AI’s ROI in claims.